Brandes Letter

June 2025

Dear Clients and Friends,

In our October 2021 letter, we highlighted how—despite being considered as a “deep value” manager by many observers—the Brandes approach to value investing does not fit neatly in a rigid style box. Rather than confining our stock selection to the cheapest-decile stocks or those traditionally labeled as “value,” we take a broad and flexible view in our search for value opportunities. Our investment universe covers companies across a spectrum—from high-quality to potentially deeply discounted turnaround prospects. Regardless of whether a stock is labeled as value, core, or even growth, if it presents an attractive margin of safety1 based on our bottom-up research process, we will consider it for our portfolios.

Staying true to our value discipline, Brandes portfolios have consistently served as a value-oriented building block for our clients across various market environments, while adapting to the evolving opportunity set. We believe our flexible, price-conscious approach has been a key driver to the absolute and relative performance of many of our strategies over the past five years. For example, our International Equity and Global Equity strategies rank in the top decile of their respective eVestment peer groups over the five-year period ending June 30, 2025.

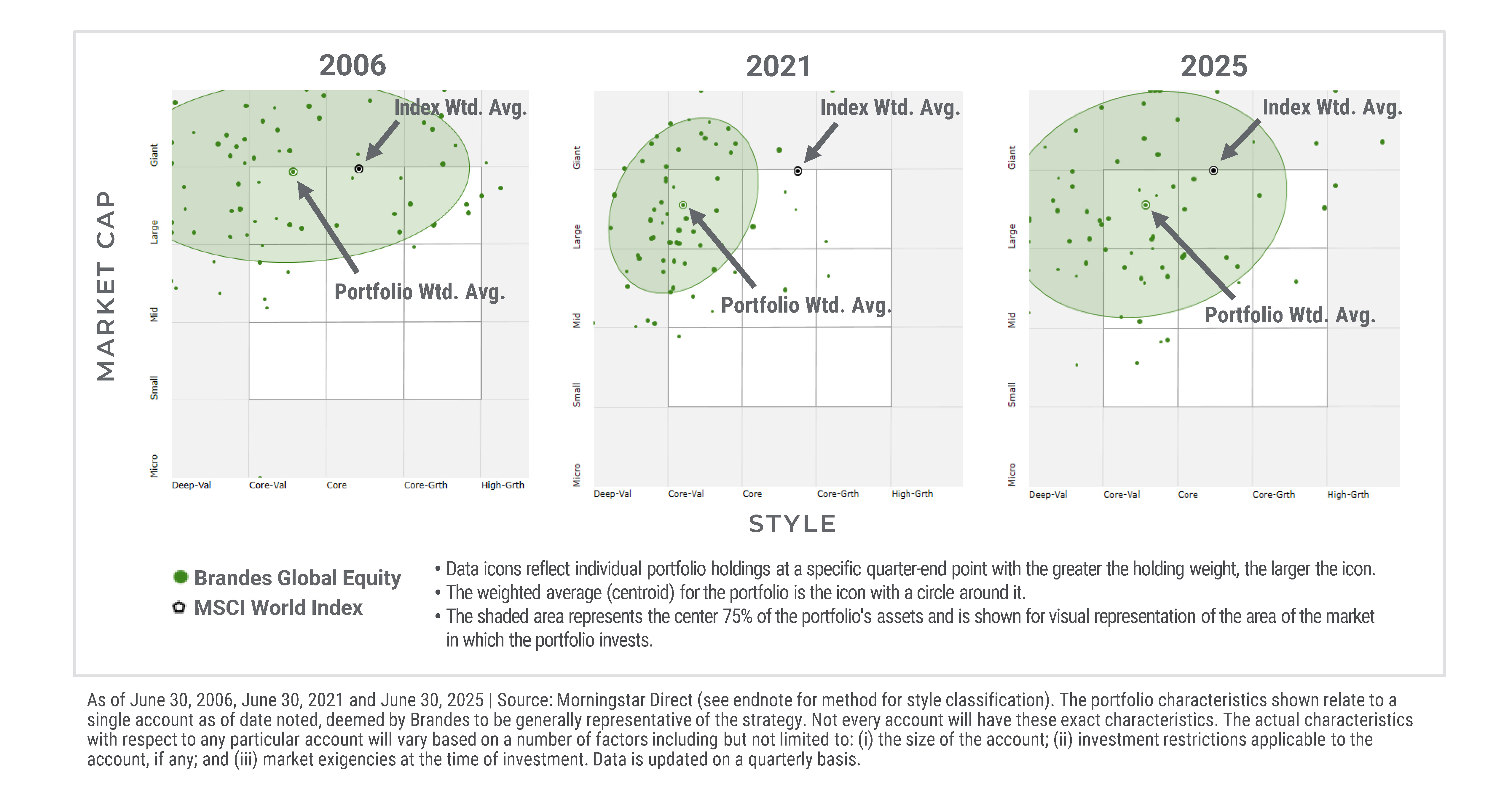

In our 2021 letter, we shared Morningstar’s holdings-based style analysis charts to illustrate how the Brandes Global Equity Strategy was positioned in two distinct market environments—2006 and 2021. To provide a current perspective on the evolving opportunity set, we’ve added a 2025 snapshot. This updated view offers fresh insight into how our strategy continues to adapt across different investment landscapes.

Brandes Global Equity Value Exposure

Morningstar Holdings-Based Style Chart: 2006, 2021, 2025

The charts above demonstrate how our strategy has consistently maintained a value orientation. However, while the weighted average (centroid) of our strategy has always remained in the value quadrant, the shaded area—which represents the center 75% of our holdings—tells a more nuanced perspective.

In 2006 and again in 2025, the shaded area appears wide, reflecting a broad opportunity set across the value spectrum. In contrast, the narrower shaded area in 2021 indicates a more concentrated set of value opportunities during that period.

This visual underscores a key principle in our investment philosophy: While our portfolios are always value-oriented, the types of companies we invest in—and where they fall along the value spectrum—vary depending on the opportunity set. Our flexibility allows us to pursue value wherever it exists, whether in high-quality businesses, cyclical rebounders, or misunderstood turnarounds. Instead of excluding an investment candidate from our investible universe because it does not screen “value” based on traditional valuation metrics, we bring a business-owner mindset and make that determination ourselves.

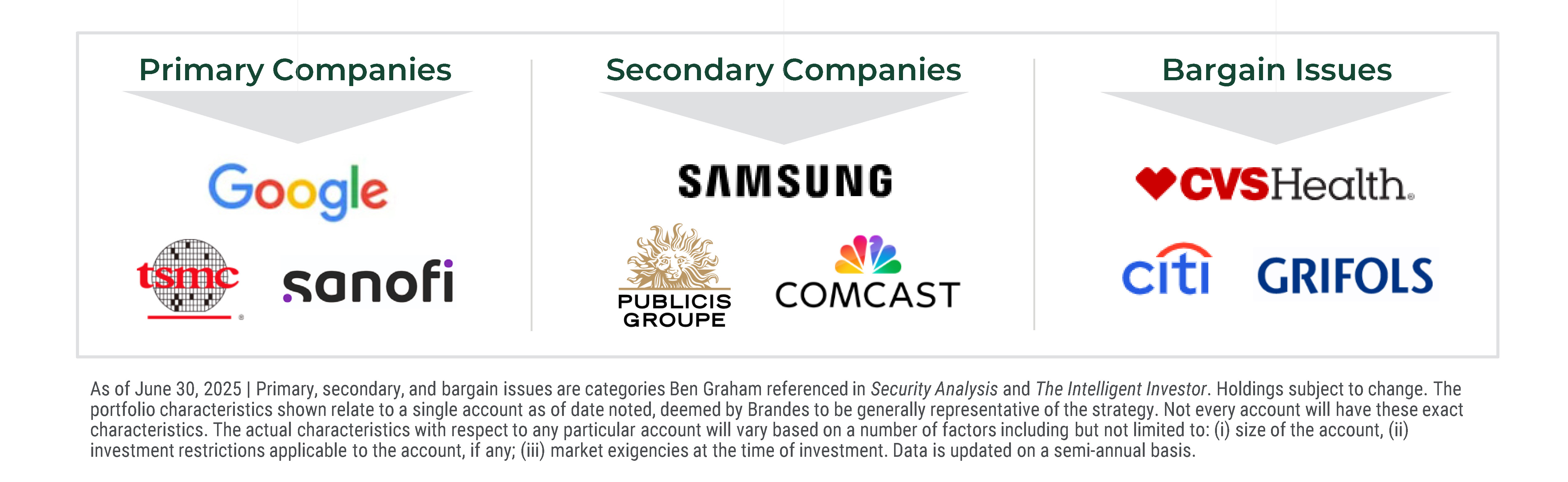

Borrowing the terminology introduced by Benjamin Graham, we view our holdings as falling into three categories: primary companies, secondary companies, and bargain issues. Each represents a different type of value opportunity and plays a unique role in our portfolios.

These are well-established businesses—often leaders in their industries. They typically exhibit consistent earnings, strong balance sheets, and durable competitive advantages. While they may not appear “cheap” based on traditional valuation metrics, there are times when the market will misprice (undervalue) these companies, in our opinion. Our broad company coverage enables us to identify and capitalize on such opportunities. When we find a compelling investment case for a primary company, we are normally comfortable owning it at a lower margin of safety given its quality and typically above-average growth potential. Additionally, primary companies may receive above-average allocations for a given margin of safety.

Secondary companies are solid businesses that are temporarily out of favor—often due to sector-wide, geographic, or cyclical factors. They may operate in less glamorous industries or face short-term headwinds, but their fundamentals remain sound. In our view, they provide a balance between business quality and upside potential. Most of our opportunities fall into this category, where valuation dislocations often create compelling entry points.

Our allocation decisions for these companies are driven by their relative margin of safety and our assessment of how quickly operational or fundamental improvements may materialize.

Bargain issues represent companies that are undergoing major restructuring or facing temporary, yet significant challenges. They may be misunderstood, complex, or simply overlooked. While they carry higher risk, they also offer the potential for outsized returns should our analysis prove correct.

We take a more cautious approach in deciding our allocations for bargain issues, being conservative in averaging down and quick to trim or exit positions as prices approach our intrinsic value estimates.

Brandes Buckets of Value – Based on Graham Principles

Sample Opportunities Across the Value Spectrum – Brandes Global Equity

Across these three sources of investment opportunities, we are guided simply by our fundamental analysis. We apply a business-owner mindset to look through a business cycle and try to take advantage of when we believe the market is under appreciating the prospects for a business. As long as we can buy a business at a discount to our estimate of its intrinsic or fair value, every business—regardless of how it’s defined in the index—is a potential candidate for our portfolios.

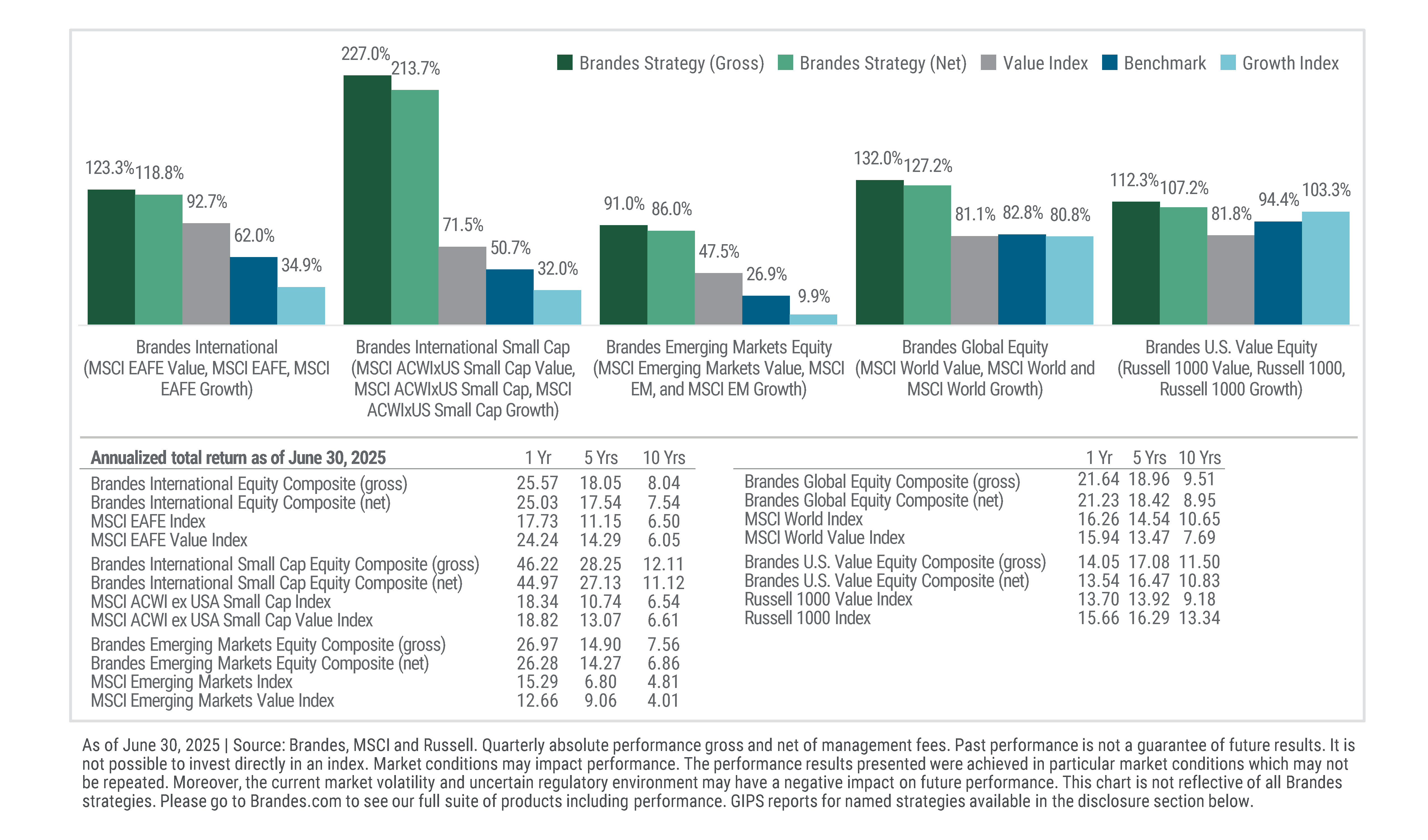

Our price-conscious value approach has not only resulted in portfolios that plot value based on their holdings, but also ones that are leveraged to value from a performance perspective. Since the value rebound in September 2020, the below strategies have performed well, outperforming both the broader market and the value indexes on a cumulative basis.

Returns During Recent Value Rebound – Since September 2020

Compared to Benchmark, Growth and Value Indices (Cumulative)

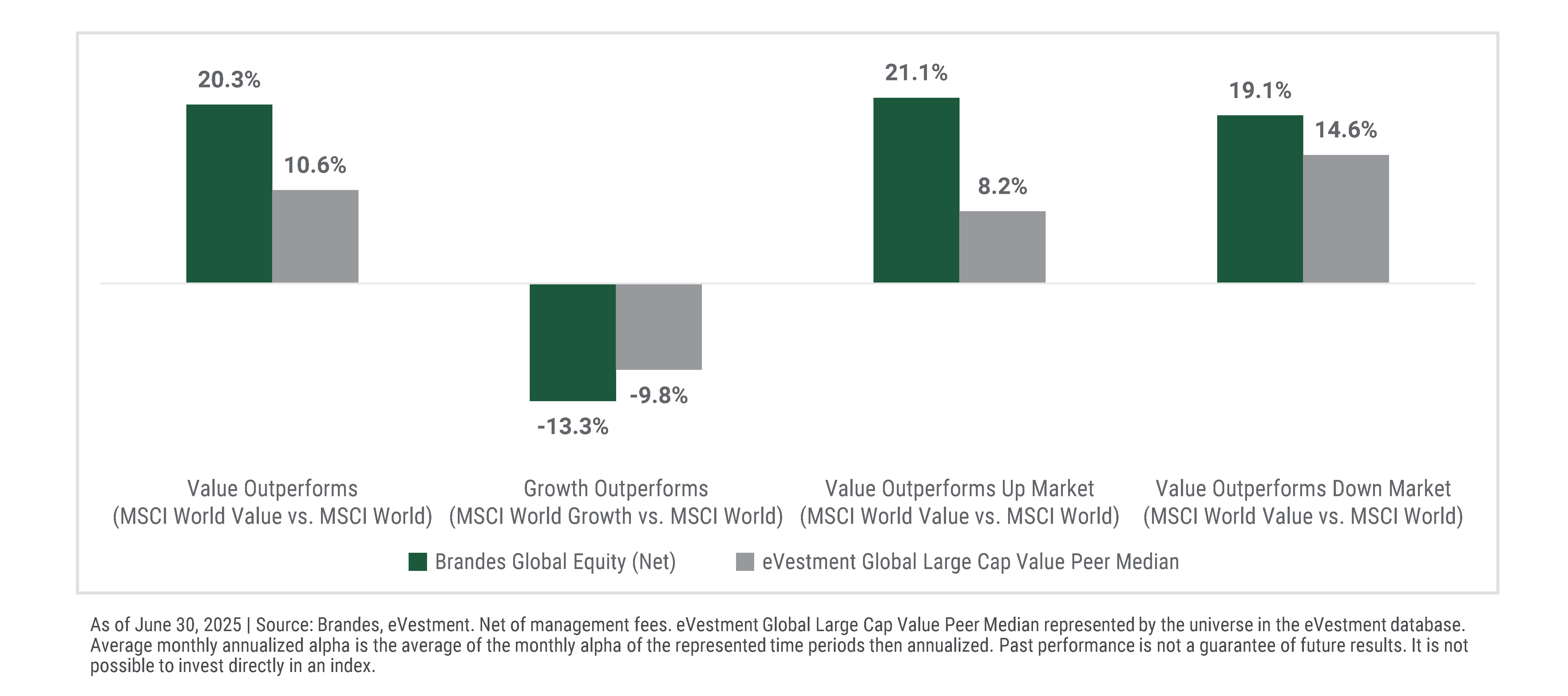

While past performance is not a guarantee of future results, the recent performance is consistent with the historical return pattern of our portfolios: When value investing has performed well, Brandes strategies have tended to do well. As exemplified in the chart below, our Brandes Global Equity Strategy has shown a tendency to outperform peers during value-led market cycles. Over the past 10 years, when value outperformed the broader market (MSCI World Value vs. MSCI World), the Brandes Global Equity Strategy outperformed the MSCI World Index by 20.3% on average (based on monthly annualized alpha). In our opinion, this leverage to value is a natural outcome of our disciplined, research-driven process.

Brandes Global Equity vs. Peers

10-Year Average Monthly Annualized Alpha (vs. the MSCI World Index)

Our consistent value orientation—as highlighted by the Morningstar's holdings-based style charts above—shows that while we are always firmly rooted in value, we are not constrained by narrow definitions. Our flexibility allows us to pursue opportunities across the full value spectrum, including primary and secondary companies, as well as bargain issues. The result is portfolios diversified across the value spectrum that, in our opinion, balance quality, valuation, and potential upside, while having had the tendency to do well during value-led cycles, such as the one we have observed in the past few years.

We remain committed to this price-disciplined, research-driven approach and believe it will continue to serve our clients well in the years ahead.

Thank you for your continued trust and partnership.

Sincerely,

Brandes Investment Partners