With our disciplined and repeatable fundamental value investing approach, it may not be surprising that the Brandes Global Equity and International Equity strategies are levered to value—meaning they have tended to outperform their benchmarks when value stocks lead. But how much leadership from the value style is actually required for Brandes strategies to do well?

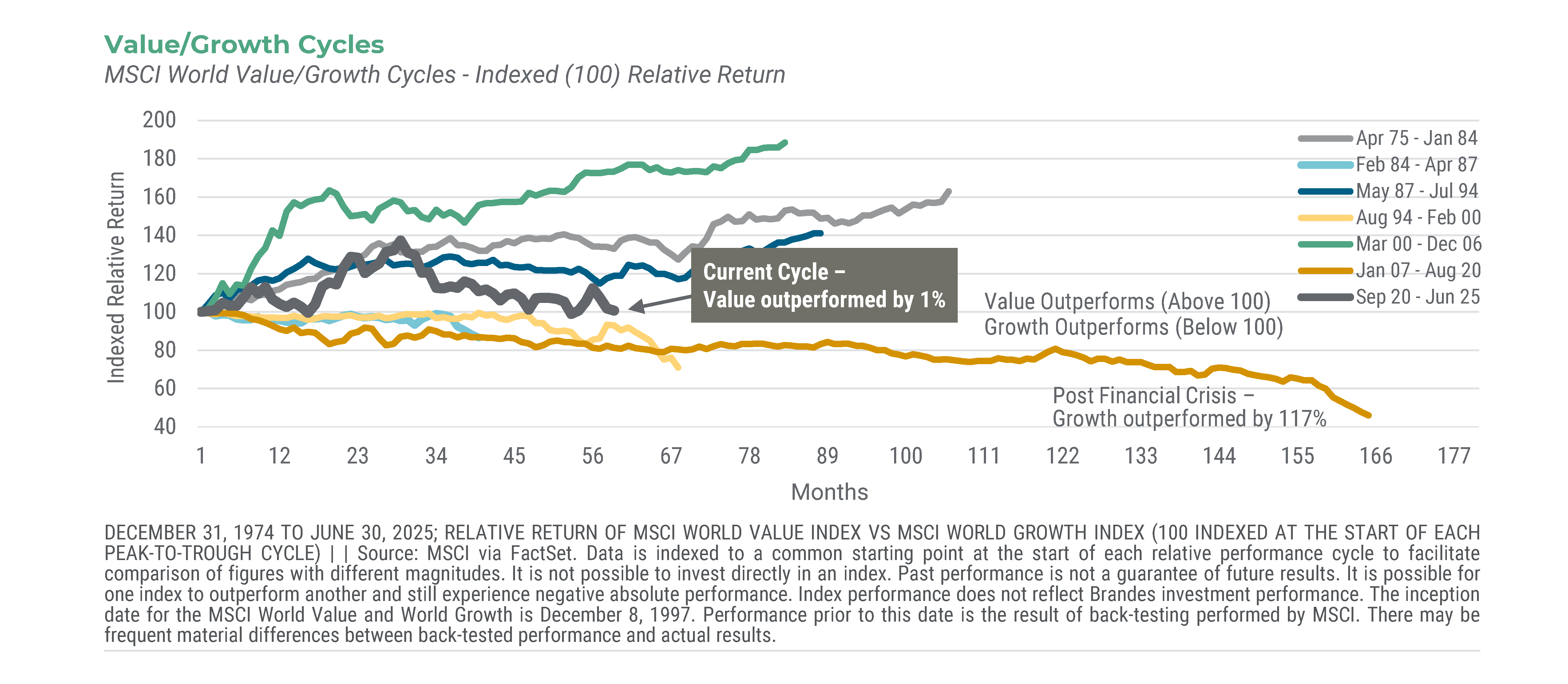

Pfizer Monday in late 2020 marked a turning point for value stocks,1 ending growth stocks’ longest stretch of outperformance in history and ushering in a resurgence in value. While value has led since then, the path has been volatile and the performance gap has been narrow: For the period from 9/30/20 to 6/30/25, value outpaced growth by just 1% cumulatively (MSCI World Value vs. MSCI World Growth).

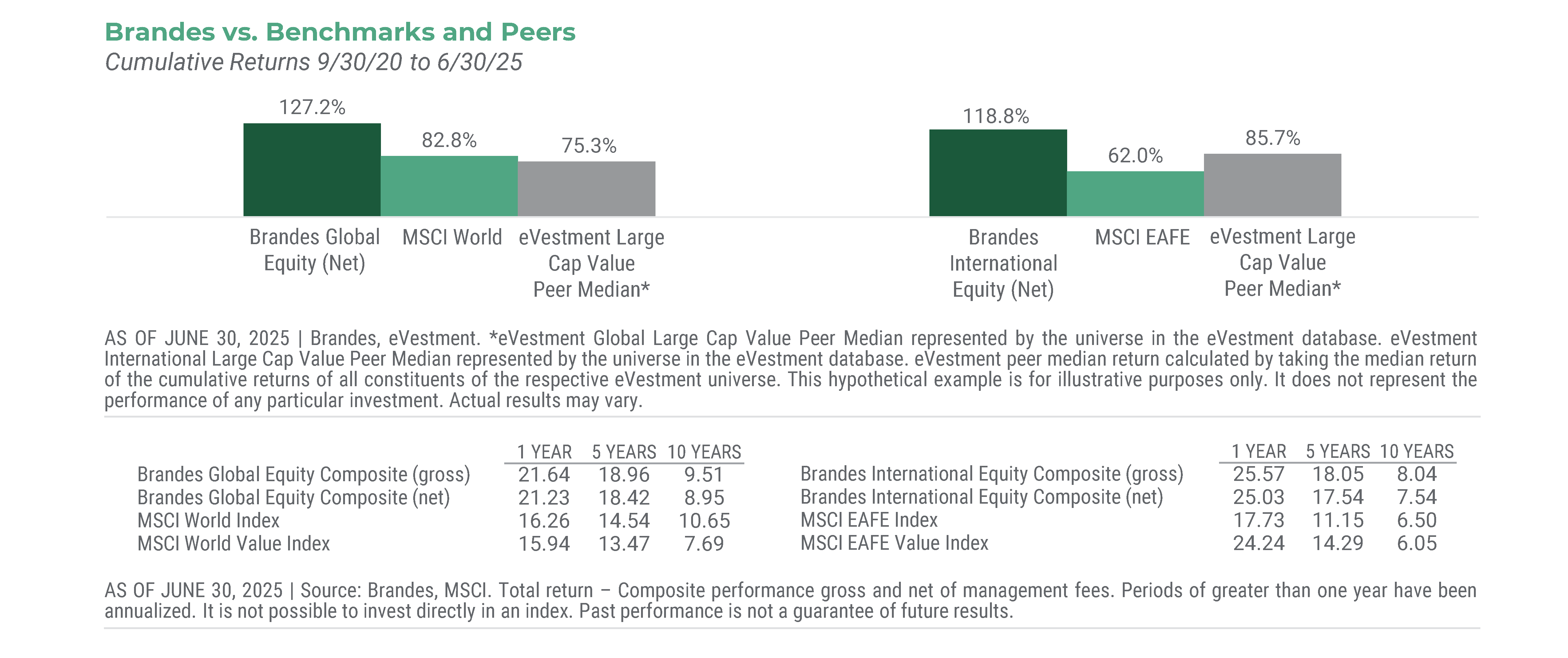

Yet, despite this modest margin, the Brandes International Equity and Global Equity strategies have exceeded their benchmarks, while also performing better than its eVestment peer medians. In our view, this reflects the strength of our bottom-up stock selection process.

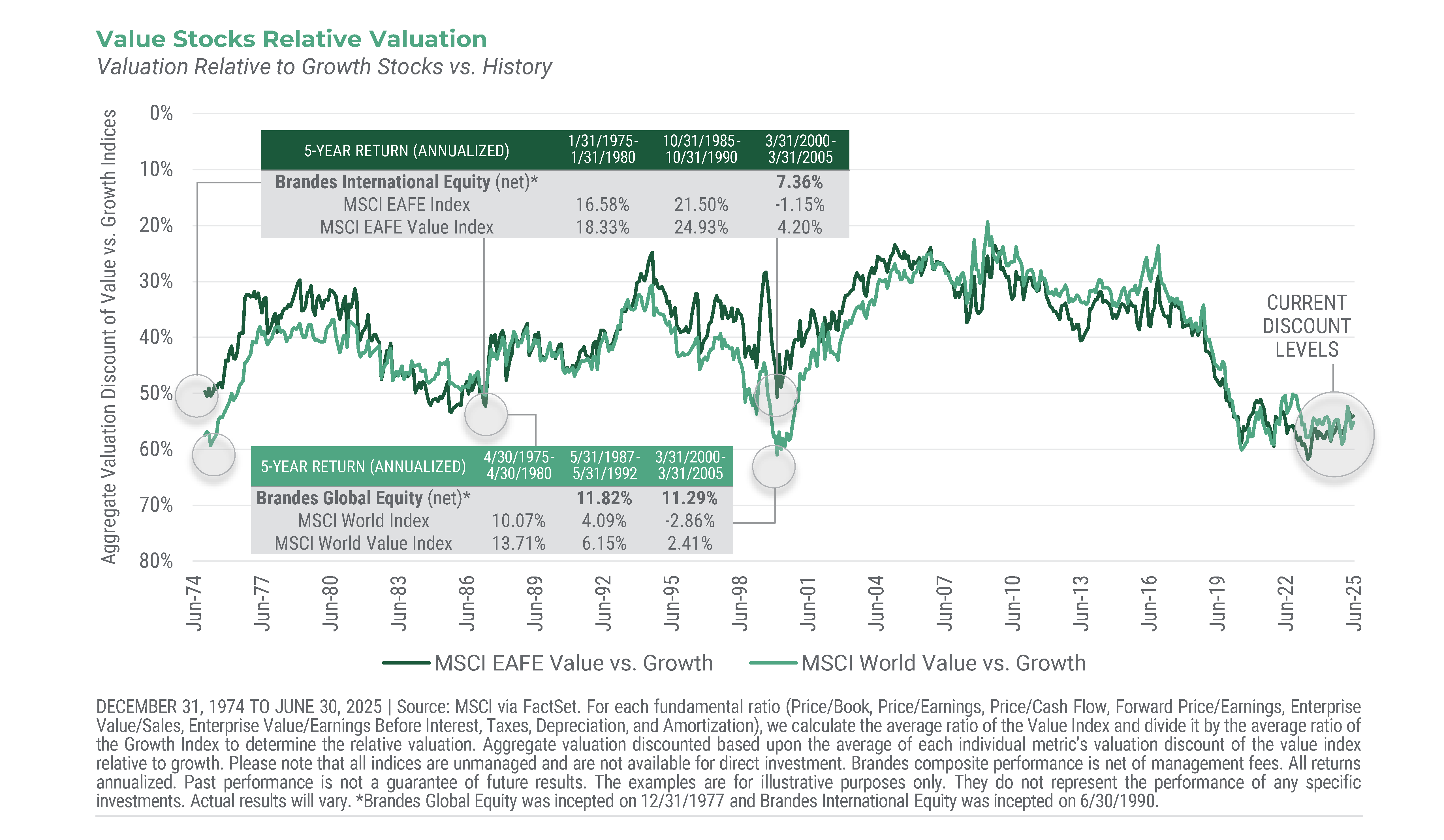

As of June 30, 2025, value stocks traded at historically low valuation levels compared to growth stocks—across both the MSCI World and MSCI EAFE indexes. This is encouraging to us as such discount levels have tended to precede attractive relative returns for value.

We believe there is a meaningful runway ahead for value to continue its momentum. Given our strong leverage to value, we’re excited about the prospects of our strategies.