Chris Duncan is a Director, Investments Group, a Senior Analyst on the Basic Materials Research Team and a member of the Small-Mid Cap Investment Committee. He is a limited partner of the firm’s parent company. Before joining the firm, Mr. Duncan was as an M&A Analyst with NCR Corporation. He earned his BS in finance from the University of Dayton and his MBA (with honors) from the University of Chicago Booth School of Business. Mr. Duncan’s relevant experience began in 2001 and he joined Brandes Investment Partners in 2006.

Amid dynamic changes in the energy sector and the unpredictable nature of commodity prices, we spoke with Chris Duncan, CFA, to understand the complexities of investing in oil and gas companies. He addresses the challenges of forecasting oil prices, the qualities that make certain companies more resilient, and the factors affecting long-term hydrocarbon demand. Chris also shares where Brandes has found value potential in the industries and countries in the energy sector. He has been with Brandes since 2006 and has 23 years of industry experience.

First, you never really get comfortable investing in them if you truly understand the volatility and uncertainty involved. However, perhaps we should consider the actual impact of accurately predicting oil prices on investment returns. Many people view this as a key determinant of whether owning oil and gas stocks will yield attractive returns.

Let’s start with this example: Suppose you were to look at a large-cap U.S. exploration and production (E&P) company and forecast that oil prices next year will be 20% higher than this year. The direct impact on the company's value is relatively minimal. If you calculate a 20% increase in the price per barrel, which amounts to about $15, and multiply this by their production volume, the increase in value, calculated as a percentage of market cap, would be less than 2% for many large-cap E&Ps.

Consider another more pronounced example dating back to 2006, when oil prices were at $60, having averaged around $35 in the previous five years. At that time, U.S. oil production had been declining almost every year since 1985, and Exxon was contemplating building a natural gas import terminal in the U.S. Despite predictions of a peak in global oil supply, as suggested by a book popular among energy analysts called Twilight in the Desert, some investors might have predicted higher future oil prices and a potential increase in U.S. oil production due to emerging shale extraction and hydrofracking techniques.

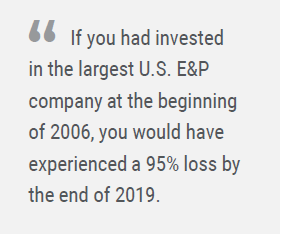

If you had invested in the largest U.S. E&P company at the beginning of 2006, you would have experienced a 95% loss by the end of 2019. Investing in the second largest E&P would have resulted in a loss of over 65%, and the third largest would have seen a 50% loss. Despite these outcomes, your investment assumptions might have been based on sound reasoning, considering that oil prices averaged $75 over the subsequent 14 years and U.S. oil production grew 6.7% annually during that period.1

However, even with these favorable conditions, losses were significant. To find a relatively better outcome, you would need to look at the seventh-largest producer, which boasted superior acreage, management, and capital efficiency. This company managed to grow its production by 9% annually for 14 years. Despite this impressive growth, an investment in this company would still have underperformed the S&P 500. Moreover, if you had bought an index of U.S. E&Ps at the beginning of 2006 and held it throughout this period of significant production growth and higher than average commodity prices, you still would have significantly underperformed the broader market. This demonstrates that despite this knowledge and understanding of oil price dynamics, a favorable investment return is not guaranteed.

The primary characteristic I consider as an investor is the price implication offered by the market. We evaluate companies by considering several factors, including the commodity price cycle, which plays a role in valuation but is not the dominant factor. We assess the company’s growth prospects, such as their resource base and opportunities to redeploy capital for growth. We also consider the capital efficiency of this growth, how much they earn back by redeploying capital from their resource base into new resources, and what the market implies about the cost of equity and capital. The more conservative the market's assumptions on these variables, the more confidence we have in the investment. We look for companies with the right pricing and the ability to survive any market cycle due to their robust balance sheets, low financial leverage, and low operating costs, allowing them to manage through downturns and grow.

For an upstream company whose business primarily involves producing oil and gas, we usually start by valuing the reserves they have already developed. The bulk of an oil and gas company’s capital is invested up front, followed by a reserve life that produces and sells in the market over subsequent years. These companies must continually reinvest their cash flows from that reserve base to replace and grow reserves. Therefore, we typically assess the value of the reserves in place, which is an element of production cost and commodity price assumptions.

However, more importantly, we look at the company's ability to efficiently redeploy these cash flows. In many pure-play upstream companies, there is a tendency to deploy capital inefficiently, so we do not typically place much of a premium on existing reserves. However, some companies possess a significantly better-quality asset base and a longer runway for capital investment and growth, which might justify a premium for their reserves in the ground.

I believe that the future will see a peak in hydrocarbon demand, although it's challenging to predict exactly when that inflection point will occur, due to two competing elements. First, there is the energy transition towards renewables, which is increasingly demanded by consumers and promoted through government regulations and subsidies. However, the pace of this transition may face challenges due to the scale of the task, the significant investment required, and the current small scale of these industries, suggesting a bumpy road ahead.

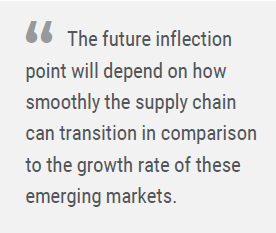

The second element is the growth in emerging market economies, which tend to have more oil-intensive gross domestic product growth. Despite consuming less per capita than developed countries, emerging markets have driven more than 100% of the global oil demand increase over the last 20 years due to their economic growth.2 The future inflection point will depend on how smoothly the supply chain can transition in comparison to the growth rate of these emerging markets. This makes it very difficult to predict. Consequently, when evaluating oil investments, we consider the sensitivity to whether this inflection point occurs around 2030 or as late as 2050, and how this timing might impact the companies we are considering for investment.

Over the past few years, we've generally seen reduced allocations to energy across our portfolios, influenced by the post-pandemic recovery, improved oil and natural gas demand, and factors such as the Russia-Ukraine conflict supporting commodity prices. Additionally, energy companies have become better at returning capital to shareholders. Consequently, there are not as many negatives associated with the industry today, and the opportunity set is not as rich for us as it was during periods of greater market panic and uncertainty.

However, we see value potential in European integrated oil companies due to their relatively undemanding valuations compared to their U.S. peers. The transition to renewable energy adds complexity to the energy markets, a factor that could create value for integrated oil and gas companies. These companies are not only involved in oil and natural gas supply but also in electricity production and trading. Their ability to operate across various energy forms and geographies, a characteristic more pronounced in Europe than elsewhere, could take advantage of the increased market complexity.

If we go down the capitalization spectrum, the quality and efficiency in capital deployment tend to diminish. These companies are less diversified and face more secular risks, such as the maturity of their core areas. Therefore, our exposure here is more limited. We invest in some oilfield service companies, which are typically late-cycle beneficiaries of industry uptrends in commodity prices and capital expenditure. Therefore, their results have yet to see the positive impact that we expect as we go through the cycle. Additionally, we hold positions in U.S. natural gas companies, which remain competitively positioned on the cost curve. The prospects for these companies to be able to deploy capital efficiently are high, and U.S. natural gas prices are depressed following a strong performance in 2022. Therefore, we’re still seeing some value opportunities there, though our options are somewhat limited within our investment universe.