Dear Clients and Friends,

At Brandes, we are gearing up to celebrate our 50th anniversary in 2024. Since our founding, we’ve seen a lot of market cycles. We’ve experienced robust periods that required us to close all our strategies to new deposits to preserve capacity for our existing clients. We then saw a decade plus of growth investing dominance, during which many in our industry were convinced that value investing was dead, and the core principles of value would never work again. However, with almost five decades under our belt, we believe that the culture we’ve built, the infrastructure we’ve carefully assembled, and the people we’ve selected to work with us have allowed us to deliver on our promise to our clients—to endeavor to provide consistent and reliable exposure to value in their portfolios.

Investing is a people business, and we believe Ted Kim, our automotive analyst, embodies the attributes of independence of thought, a diversity of background and experiences, and a calm temperament that we think are essential qualities needed to stay dedicated to value investing through good and bad times.

Ted is a soft-spoken, thoughtful value investor who came to the United States from South Korea when he was 12 years old. He is a self-professed student of the automotive industry and reads constantly about the companies in the industry and its changing customer preferences. Over his many years in the business, he has seen massive changes. He recently noted: “The advent of electric vehicles (EVs), the emergence of Tesla, and the fall from dominance of the traditional Big 3 automakers in the United States are multi-year seismic shifts that I believe have a profound impact on how a long-term investor should evaluate companies in the industry.”

In a typical year, Ted consumes hundreds of sell-side research reports and articles written by industry experts and consultants, listens to industry-related podcasts, and interacts with C-suite executives of automotive companies on various continents. He also attends several major industry conferences each year. All of this helps him to stay on top of potential opportunities and threats within the industry. Ted explains that: “Reading reports and listening to podcasts helps me stay informed about the industry and its trends, while attending conferences and interacting with C-suite executives provides me with insights into operations, strategic initiatives, and competitive positioning of the companies in the industry.”

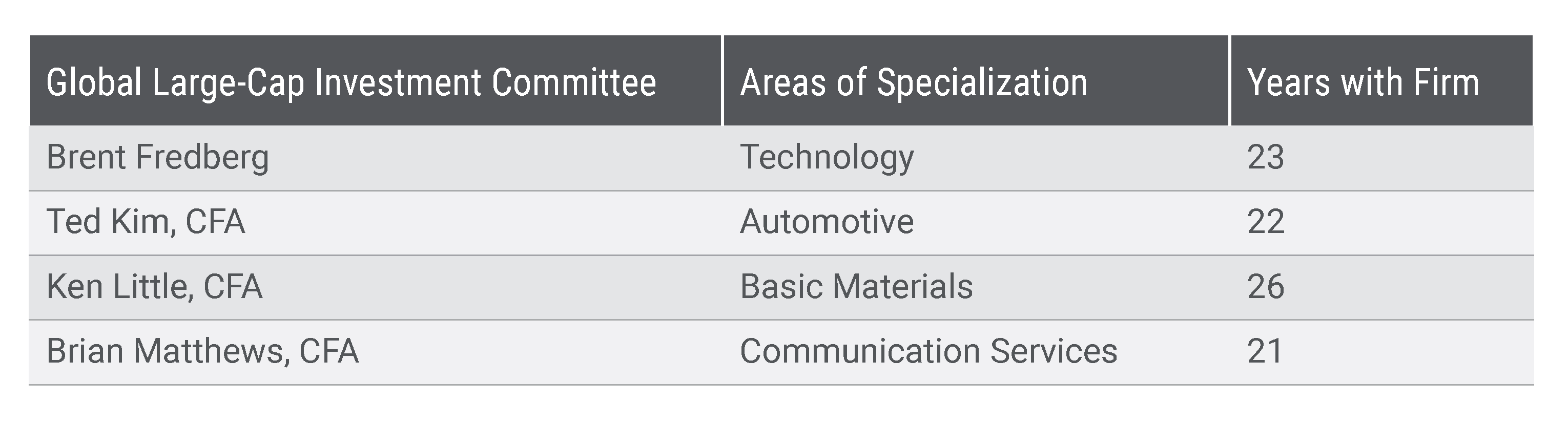

Like many of our investment professionals, Ted wears a few hats when it comes to managing portfolios for our clients. Ted is a Team Leader, an Analyst, and an Investment Committee member.

Every month, our Managing Director of Investments, Ken Little, and our sector team leaders meet to discuss industry insights, news flow, and relevant factors impacting each area of coverage. This meeting serves as a vital feedback loop, formalizing communication from the investment committees to our research analysts. During these discussions, team leaders review workload and adjust analyst resources as needed. This helps ensure that every sector receives the attention it deserves, and our analysts can then focus on identifying the best investment candidates from around the world for our investment committees to consider.

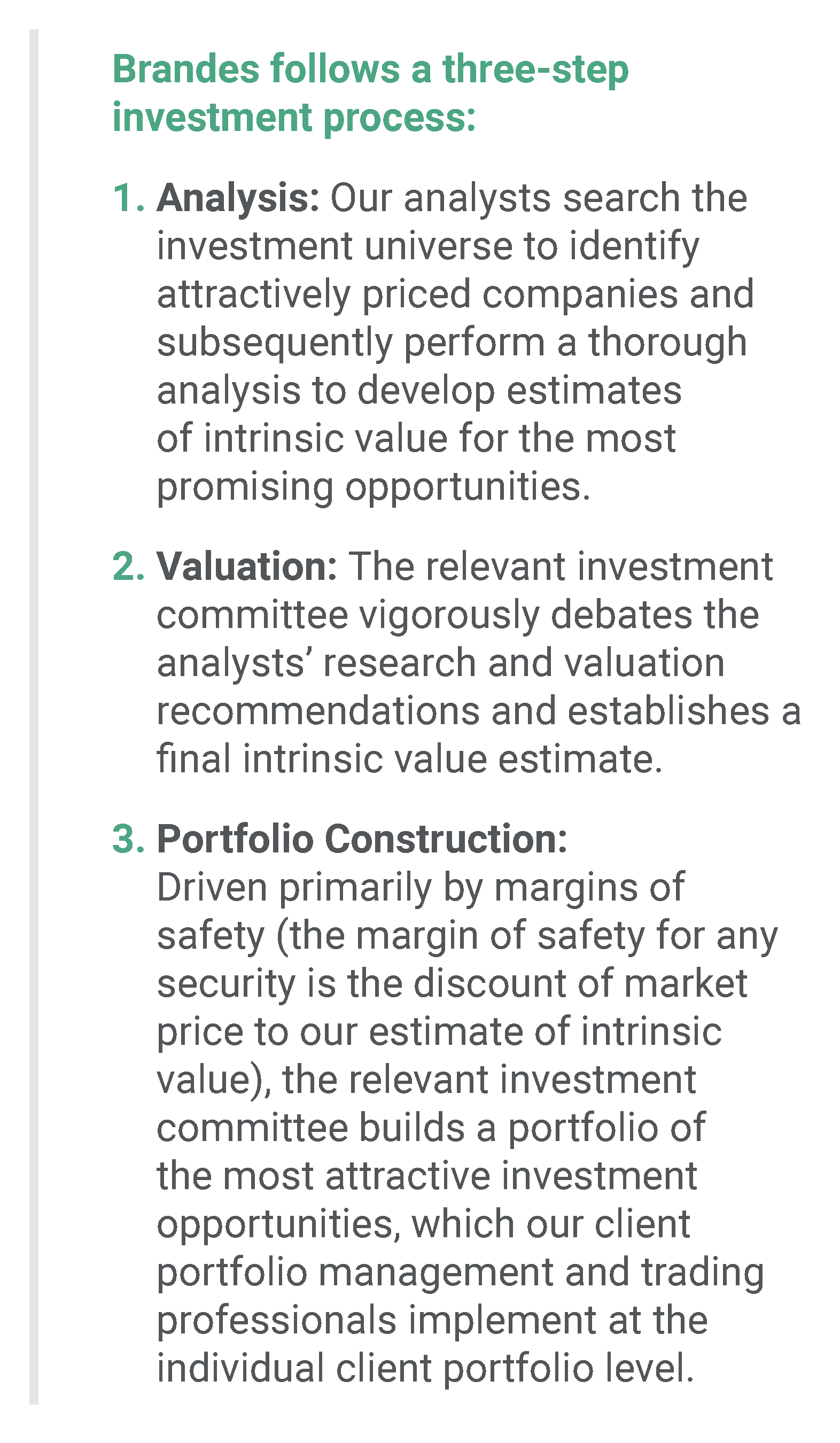

Our investment process begins with the rigorous screening of potentially undervalued companies using a variety of metrics customized for each sector and industry. These metrics may include commonly used data points such as price/earnings, price/cash flows, price/book, and enterprise-value-to-free cash-flow ratios but often include more industry-specific metrics. For example, our financials analysts may focus on adjusted book value and net interest margins when examining a bank, while our health care analysts often consider enterprise value plus capitalized research and development when evaluating a pharmaceutical company. Our analysts generate ideas from a variety of sources, including meetings with management teams, presentations at investment conferences, monitoring industry news, examining external research reports, and suggestions from team leaders and investment committee members. This ensures that our potential investment opportunities are thoroughly vetted before undergoing rigorous analysis.

Our analysts then conduct extensive research on these potential investments to statements and other publicly available information to gain a deep understanding of a company and often interview management teams to gather quantitative and qualitative information that help them develop a long-term outlook for the company. Although Ted is our resident specialist on automotive companies, he relishes sharing his detailed work with his colleagues on an investment committee. According to Ted, “Having my work peer reviewed by colleagues who I know to be seasoned value investors is really a rigorous devil’s advocate process. They challenge my work, they poke at my assumptions, and ultimately, they make me a better analyst. Because of this investigation and debate that takes place for every stock, I know that my assumptions need to be supported with data, and the investment case presented clearly with all the major positives and potential risks taken into consideration. I think our clients are well served by this important step in our process. I am a firm believer that two heads are better than one and, in our case, three to five heads are even better still. In addition, as pragmatic investors, we understand that there is not a “one-size-fits-all” formulaic approach to valuing businesses. Across sectors, we routinely apply multiple valuation approaches to triangulate and validate our fair value estimate of a candidate for investment. Our structure is designed to embrace this approach.”

At Brandes, our analysts are tasked with doing thorough, objective research to help the investment committees estimate the fair value for a business. Our analysts don’t have to obsess about getting their “picks” into the portfolio, as they are evaluated principally on the quality of their work. According to Ted: “This helps remove personal biases that could come into play when an analyst is motivated to get a certain number of “picks” into the portfolio.” Therefore, this approach allows analysts to keep a sharp focus on producing the best possible analysis and providing the most accurate assessment of a company’s fair value. This structure also means that analysts can be equally effective by helping the investment committees avoid companies and areas where opportunities are not attractive.

We believe thorough research and analysis is key to making informed investment decisions. Our investment committees, which formally meet once each week, are made up of experienced professionals who bring a diverse range of perspectives and experience to the table. They work together to carefully review and investigate the research and valuation estimates produced by our analysts. During the Valuation stage, the investment committee members engage in a deep-dive discussion and investigation to arrive at a final intrinsic value estimate for each potential investment. This process is designed to deepen their understanding of the businesses and increase their conviction in their fair value estimates. It is also a forward-looking process, considering the company’s fundamentals and drivers of value rather than solely relying on statistical models that are backward-looking.

Investment Committees

In the Portfolio Construction stage, the investment committees examine existing and potential investments from an overall portfolio perspective, with a primary focus on margin of safety. Target weightings for individual securities are also driven by margin of safety, with the larger allocations typically given to investments that offer greater margins. Other factors, such as material ESG (environmental, social and governance) issues and diversification guidelines, may also influence the allocation decisions.

With his investment committee hat on, Ted has to look beyond his automotive specialist role and play a portfolio manager role. When asked about the investment committee role, Ted was keen to stress that “Collectively and individually, we have been in this business for multiple decades. We’ve seen many different market cycles and we’ve learned a few things along the way. I really appreciate the investment committee structure and prefer it over a single manager approach. This is a humbling business, and your investment style can be out of favor for long periods of time. Keep in mind that the recent growth cycle lasted for almost 15 years (January 2007 to November 2020). In tough periods like that, it’s difficult for any individual to remain committed to an investment process. There are natural human tendencies that encourage you to just do something different, make a change, or succumb to ’it’s different this time’ mentality. I personally find a lot of comfort in being able to talk through these issues and concerns with a group of colleagues who I respect and whom I know to be solid value investors. The team dynamic and the psychological support that the group provides allows us to maintain an unwavering and sharp focus on delivering consistent exposure to value. I like that I can confidently say to our clients that while value may cycle in and out of favor, you can be sure that your Brandes portfolio is firmly focused on value.”

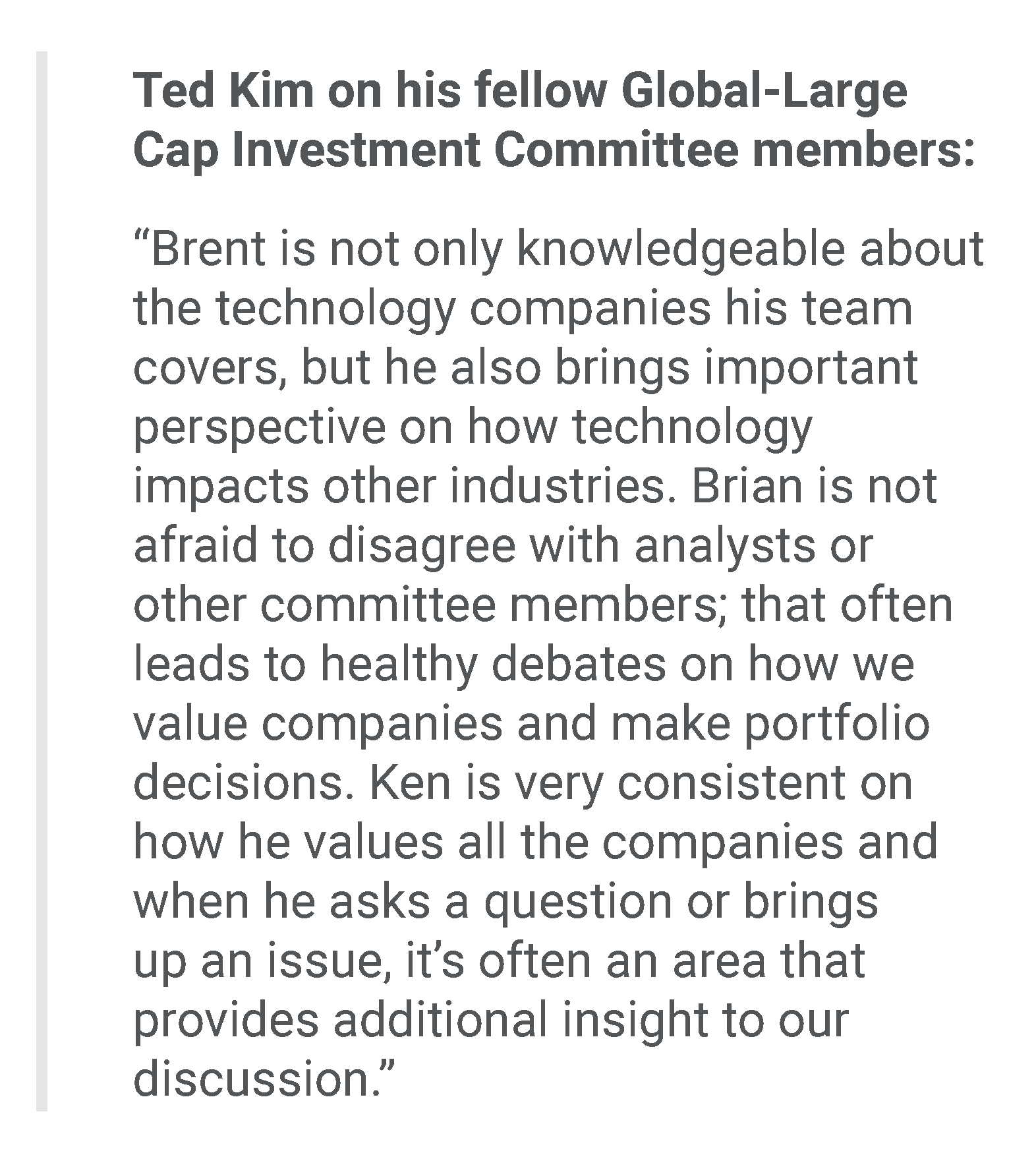

We believe that our clients benefit from a team approach to building portfolios. In addition to the potential benefits that Ted mentions, we think that having analysts serve on investment committees leads to better overall outcomes. Each committee member brings his or her own knowledge and experiences to the decision-making process. For example, Ted’s area of specialization brings important insights into valuing cyclical businesses whereas other committee members bring different areas of specialization. When asked about this, Ted mentioned: “My fellow investment committee member, Brent Fredberg, is highly knowledgeable on technology companies and is immersed in the issues affecting that broad industry. Over the past few decades, the product of the automotive industry has shifted from being solely a mechanical product to one that now sits alongside a very advanced computer. As a result, the automotive industry has become much more technology focused and intertwined with factors and issues Brent has been integrating into his fundamental work for years. Having the ability to hear his perspectives helps me to identify important issues when valuing a car company and I am convinced that our clients benefit from this diversity of experiences and insights.”

Since we’ve introduced you to Ted, we should give you some of our perspectives on the automotive industry and make a few comments about Tesla as the leading electric vehicle company in the industry. Tesla is not currently in any of our portfolios and given its current valuation characteristics, it’s unlikely to be anytime soon. Nonetheless, Ted still follows Tesla closely and seeks to understand the issues relating to the company’s valuation. Ted commented that: “Given its dominance in the global EV market and its sometimes-unorthodox approach to issues such as pricing and future product launches, it’s important that I try to understand the business since what Tesla does will likely have a big impact on other companies in the sector.”

The bull and bear case for Tesla is well documented across the financial media. However, we thought it might be helpful to understand how having a view on Tesla can assist us in investing elsewhere in the sector. For instance, in recent months, Tesla has bucked the trend in the industry: While most players are trying to hold firm on prices, Tesla has started to discount its prices in order to grow its market share. The firm may or may not be successful with this strategy, but regardless of that outcome, this has implications for all the other car companies—both EV-focused and traditional. Therefore, when we are valuing other automakers, we need to pay greater attention to their pricing strategy and consider a range of potential scenarios. What if the company slips into a pricing war? What if they have to offer discounts or low/zero interest-rate financing deals? Zero-percent financing is one thing when you can borrow at close to zero interest rates, but it is an entirely different thing in a rising interest-rate environment when borrowing costs are much higher.

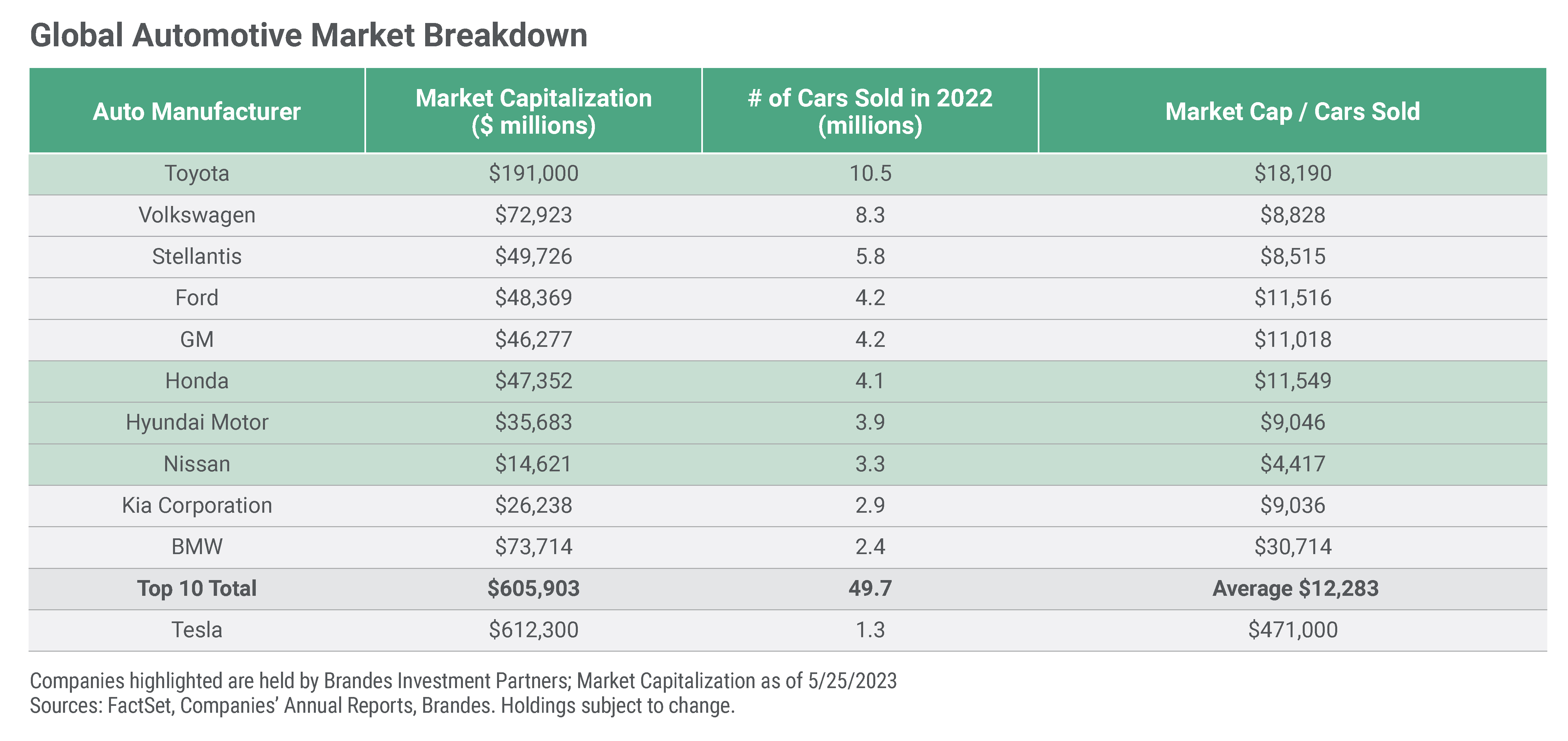

On Tesla, Ted makes the following observations: “At current valuations, Tesla would need to increase the number of cars it sells each year from around 1.5 million to the 10-15 million range and remain as one of the most profitable automobile companies to justify its current price, in my opinion. This implies that Tesla will become possibly the largest car company in the world (based on the number of automobiles sold) in less than 10 years.”

To put some perspective on Tesla’s current valuation, the following table highlights the top 10 auto manufacturers in the world, based on 2022 autos sold and compares their existing market capitalization to that of Tesla. As of this writing, the market capitalization of Tesla was roughly equal to the total combined market capitalization of these 10 leading automotive companies even though they sold approximately 38 times more cars in aggregate than Tesla in 2022.

Note that Ted is not making any judgement on the quality of Tesla’s cars or the brilliance of Tesla’s management team. Rather, he’s applying simple yet powerful logic to the investment equation. At its current stock price, Tesla needs to be selling approximately 7-10 times more cars in less than a decade in order to justify today’s valuation, from his perspective. The bulls have argued that it is not all about volume and that Tesla will find other revenue opportunities such as FSD (Full Self-Driving) features that are highly profitable. That may happen, but given the large purchase price of a car, such extra costs have not been widely accepted by consumers in the automotive industry. It remains to be seen whether such approaches will become more mainstream and, if so, whether such opportunities will be available for other automakers as well. When deploying client capital to an investment, we want to have confidence that it can generate an adequate return on that investment. One simply has greater confidence when you can buy a company at a discount to its estimated fair value than one where everything must continue to go right and, in the case of Tesla, continue to dominate its sector for the next decade and longer.

Continuing his comments on Tesla, Ted observed: “While it’s possible that sales increase tenfold or other revenue opportunities materialize, I don’t think it’s likely to happen as quickly as the market anticipates. Therefore, despite being a dominant player in the EV space and offering an excellent product, the business and the financial metrics are such that the current valuation is not, in my opinion, justified. As dyed-in-the-wool value investors, the price one pays for a company is key to us. Over time, we typically get the opportunity to purchase great businesses for less than what we believe is their fair value and we will also invest in decent businesses if we can purchase them at a significant discount to estimated value. What we will never do is knowingly buy a business for more than we think it’s worth as we believe this would place too much downside risk on our client’s capital.”

This discipline—striving to never overpay for a business—is important to value investors. If the market loves Tesla and bids up the price, other businesses in the sector may get overlooked and trade at a discount to their fair value estimates. Ted describes this discipline as follows: “It’s intuitive to me that it’s less risky to buy a company that trades at a discount to its fair value than to buy a business that is trading above its fair value. As value investors, we love investing when we can see a discount to fair value—we call it the “margin of safety” or MOS. The bigger the MOS, all else equal, the more attractive the potential investment. No matter which way I value Tesla today, it is difficult to make the case that there is currently a margin of safety. Of course, other investors employing a different investment philosophy may disagree, but in our view, Tesla is not appropriate for a value investor’s portfolio at this time. However, in the fullness of time, we’d be happy to buy Tesla if it offers an attractive margin of safety.”

In contrast to Tesla, select legacy automakers’ stocks trade at single-digit multiples of earnings, which imply that they could face declining profits and or limited growth. While, in our opinion, the current level of profitability caused by high car prices and low inventory is not sustainable and that the transition to a market dominated by electric vehicles will be costly and difficult to navigate, we also believe that the market’s view is too negative for some companies. A growing number of legacy automakers have shown that they can design and sell competitive electric vehicles and their strong balance sheets should allow them to make the necessary investments to remain competitive. Based on current stock prices, just maintaining the current level of sales volume and historical average margins could cause their valuations to increase substantially because the assumptions imbedded in the current stock prices are quite low. In analyzing and investing in the legacy automakers, we are careful in terms of selecting companies that we believe have adequate resources to compete effectively in key markets as well as realistic strategies to remain profitable companies in the future.

At Brandes, we firmly believe that investing is a people business. We have built an environment and culture that fosters the development of investment professionals like Ted Kim, who embody the temperament we believe is needed to consistently build value portfolios over the long term. Our investment process is driven by the experience and research of our analysts, who support our investment committees in building portfolios of what we consider attractively valued businesses. This process helps ensure that our investment decisions are based on rigorous research and debate, and that our portfolios are consistently constructed with a focus on value that is deeply rooted in the concept of margin of safety.

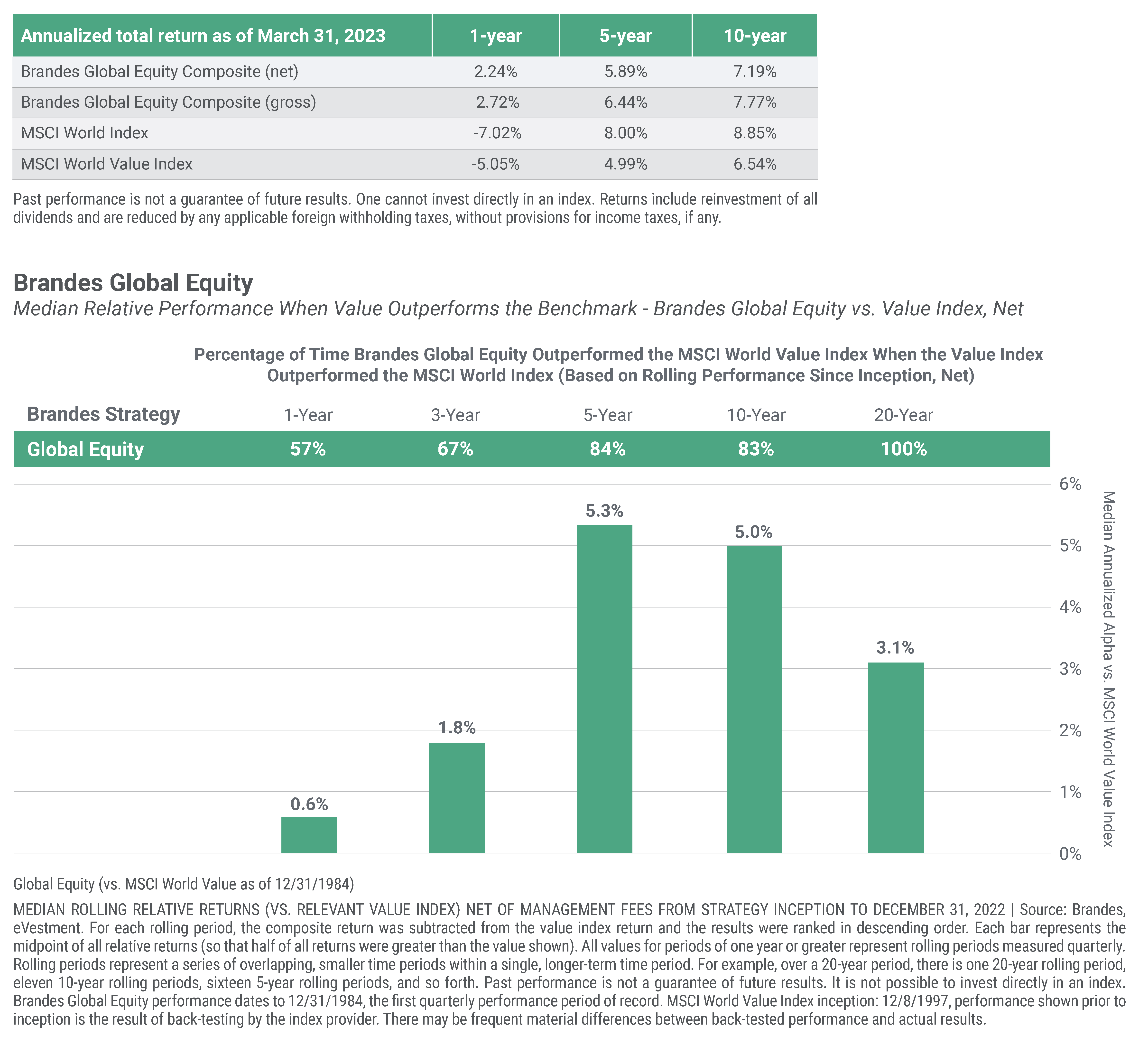

As we prepare to celebrate our 50th anniversary, we are proud to have weathered many market cycles while continuing to evolve in response to changing market conditions. We believe that our people, process, and commitment to value investing are what set us apart. When you hire a value manager, you want to be confident that when value does well your value manager does even better. We leave you with the charts below for our Global Equity strategy (managed by the investment committee that Ted Kim is a member of).

If you would like to speak with Ted or learn more about how we are purpose-built for value, please contact your Brandes relationship manager or connect with us through www.brandes.com.

Thank you,

Brandes Investment Partners