Dear Clients and Friends,

The investment world becomes more complicated by the day. We see new structures come to the market all the time. Technological advancements make it easier to manufacture increasingly complex products that use exotic financial instruments, derivatives, leverage, illiquid instruments, cryptocurrencies—and the list goes on. Most recently, we’ve seen the growth of prediction markets. While all of this is a testament to human ingenuity, does the added complexity deliver for clients in a way that justifies the added costs and risks? Does it help create long-term wealth for clients?

As a fundamental value manager, we are thoughtful about the trade-offs. We acknowledge that some of these complicated or alternative structures can meet very specific requirements of certain asset allocators. However, for many investors, the added complexity and costs may not always translate into better long-term outcomes.

We believe investing does not have to be complicated. The core idea for value investing is very straightforward: identify businesses trading at a discount to their intrinsic value, build a diversified portfolio, and give those investments time to work. What can periodically make value investing challenging is not the complexity of the approach, but the environment in which it is applied. Markets move through cycles, dominant themes, prevailing monetary policy, and geopolitical issues, resulting in different styles coming in and out of favor—often unpredictably. Importantly, our approach does not change in response to short-term market movements or sentiment shifts. We don’t panic, and we don’t overreact. Staying disciplined through those cycles requires patience and consistency more than complexity.

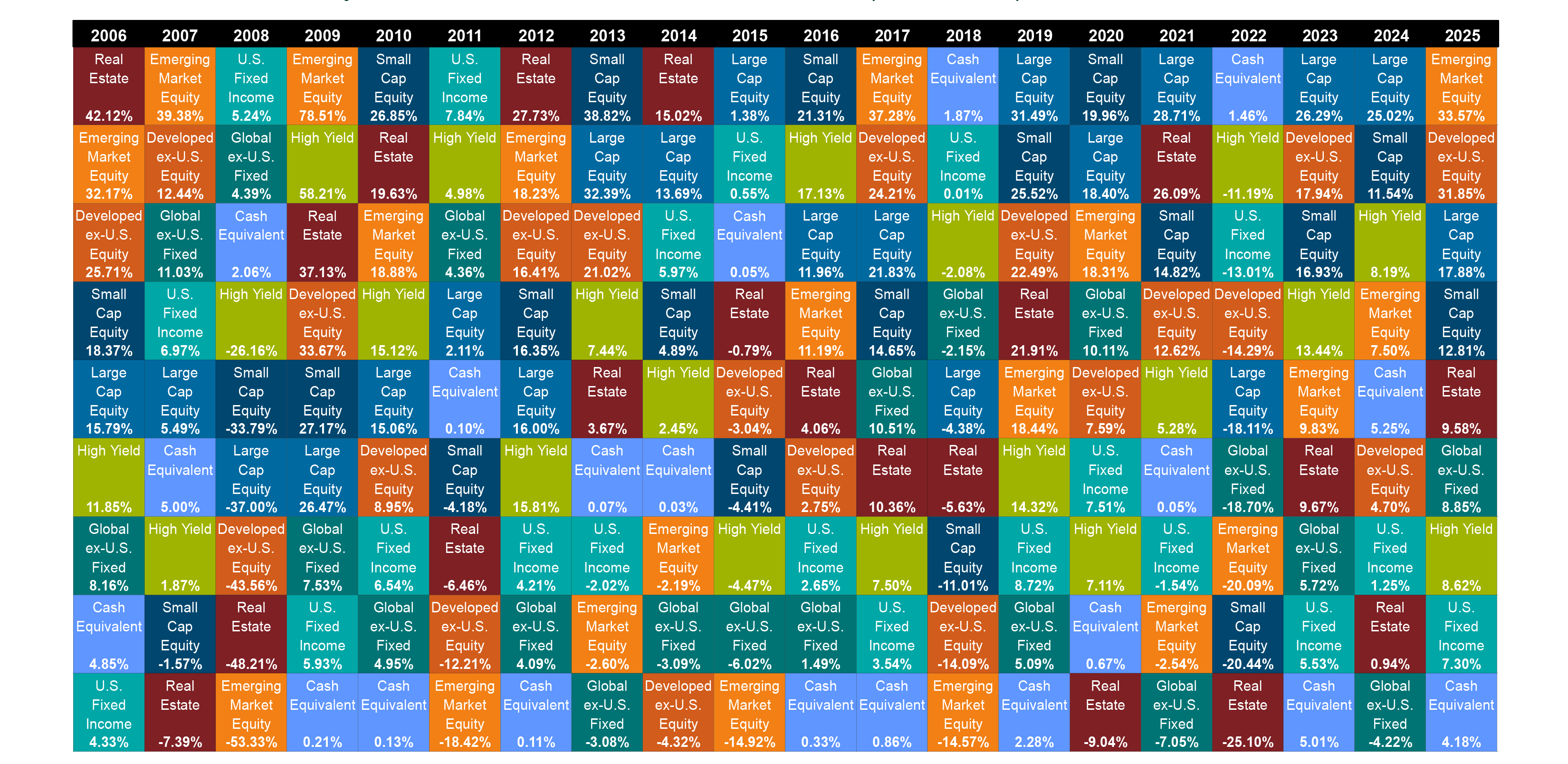

One of our favorite illustrations of the challenge of investing is the Callan Periodic Table of Investment Returns, published annually by Callan LLC. This well-known chart ranks the annual performance of major asset classes from best to worst each year. The visual message is both simple and powerful: no single asset class outperforms in every environment. Leadership rotates constantly and unpredictably. In 2025, international and emerging markets equities were the top performers; in other years, U.S. large-cap stocks, real estate, or high-yield bonds took the lead.1 This randomness underscores a hard truth that applies equally to complex strategies and simple ones: reliably predicting which asset class will win in any given year is extraordinarily difficult.

The Callan Periodic Table of Investment Returns

Annual Returns for Key Indices Ranked in Order of Performance (2006-2025)

Source: Callan LLC, The Callan Periodic Table of Investment Returns, Year-End 2025. Past performance is not a guarantee of future results. Chart is used with a written permission from Callan LLC.

At Brandes, we believe a straightforward investment framework can deliver lasting value. When the process is simple and grounded in fundamentals, conviction can be stronger.

Our flagship investment strategy is our Global Equity Strategy, with performance records going back to December 31, 1977 (inception). Since the strategy’s inception to March 31, 2026, the broad benchmark, the MSCI World Index, delivered an annualized return of 10.05%, while the MSCI World Value Index gained 9.94% annually over the same period. In comparison, the Brandes Global Equity Composite returned 13.42% gross of fees and 12.55% net of fees.

If we put this in dollar terms, had one invested $100,000 in the passive MSCI World Index back on December 31, 1977 (composite inception), they would have had $10,178,871 as of March 31, 2026. That same $100,000 invested in the Brandes Global Equity Strategy would have grown to $30,115,209 net of fees.* The power of compounding even a modest annual advantage over nearly five decades is remarkable.

Importantly, this is not alpha generated through leverage, illiquidity, or opaque structures. Instead, our discipline in fundamental value investing—applied in liquid, transparent markets—has been a key factor in helping us achieve this result.

*Source: Brandes, MSCI. Growth of $100,000 invested in the Global Equity composite from inception (12/31/77) to 3/31/26 measures the cumulative performance of a hypothetical investment, it assumes the reinvestment of dividends and other incomes. This hypothetical example is for illustrative purposes only. It does not represent the performance of any particular investment. Actual results may vary. Past performance is not a guarantee of future results. It is not possible to invest directly in an index. Please see disclosure section for important information.

The MSCI World Index was launched 3/31/1986. The MSCI World Value Index was launched on 12/8/1997. Data prior to the launch date is back tested data (i.e. calculations of how the index might have performed over that time period had the index existed). There are frequently material differences between back tested performance and actual results.

We are not saying that there is no place for alternative approaches or structures. However, the academic evidence on whether these strategies deliver superior long-term, risk-adjusted returns above public equity markets is mixed and more nuanced than is often assumed.

Some research suggests that after accounting for fees, risk, and illiquidity, the long-run return advantage of private equity versus public equity may be more modest and dependent on manager selection, access, and timing.

A study by MSCI (“Has Private Equity Outperformed Public Equity?” by Lester, O’Shea, and Warren, published in The Journal of Private Markets Investing in Fall 2025), found that since 1994 through the third quarter of 2024, buyout funds delivered an annualized outperformance of 3.8% compared to their public equity counterparts after adjusting for geography, leverage, subindustry composition, and size.2 These are meaningful numbers. However, it is important to note what these studies are actually measuring: in virtually every case, private equity—which is, by definition, an actively managed strategy—is being compared to a passive index.

The private equity manager is selecting companies, restructuring balance sheets, timing exits, and applying operational expertise. The benchmark against which this effort is measured is an index that does none of those things. A fairer comparison would be to measure private equity net-of-fee returns against a universe of skilled active public equity managers—professionals engaged in a similar pursuit of alpha, but within liquid, transparent, and accessible markets. When viewed through this lens, the return differential may be less consistent and more dependent on access to top-tier managers, particularly after accounting for fees and illiquidity.

There is also a practical reality that is often overlooked. Most research presents average or pooled results across thousands of funds, but the dispersion of outcomes in private equity is enormous. The very best private equity managers have delivered exceptional returns; however, gaining access to those top-tier managers is often challenging. They can be capacity-constrained, often closed to new investors, and typically require large minimum commitments and longstanding institutional relationships. The typical investor—and even many institutional allocators—is far more likely to end up with a median private equity fund, where the risk-adjusted advantage after fees and illiquidity may be less than expected.

In contrast, many of the world’s best active public equity managers are available to investors of all sizes through regulated mutual funds, with daily liquidity, full transparency, and more reasonable fees. In this sense, active public equity can offer many of the same benefits investors seek from alternatives: professional security selection, active decision-making, and long-term value creation without the same degree of complexity, illiquidity, or cost.

As Fama and French observed in their older, yet still relevant landmark study of mutual fund performance (“Luck versus Skill in the Cross-Section of Mutual Fund Returns,” published in The Journal of Finance in October 2010), while the average active fund may not outperform, the cross-section reveals a meaningful population of skilled managers who do, and crucially, those managers are accessible.3 Of course, there will always be outliers. For example, had you been an early investor in Amazon, you would have made outsized returns. But building an investment strategy around the expectation of identifying the next Amazon or Apple is more appropriate for “prediction markets,” and in our opinion, is not fundamental investing. Taken together, we believe these considerations reinforce a broader point: increasing complexity does not necessarily improve investor outcomes.

Complexity comes with higher costs—base fees, performance fees, transaction costs, and significant operational expenses. Higher costs mean that the investments must do even better just to deliver comparable long-term returns. Over time, the cumulative effect of higher fees can significantly erode the very alpha they promise to deliver.

Illiquid investments may offer the allure of superior returns, but they may limit flexibility, particularly during periods of market stress. Liquidity has real value, especially when you need it most.

Benjamin Graham, widely considered as the father of value investing, devoted the first chapter of his classic book, The Intelligent Investor, to what he viewed as a critical difference between investing and speculation. He wrote:

"An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative."

As regular readers of our letters will recall, we explored Graham’s enduring relevance in depth in our March 2022 Brandes Letter, "The Enduring Value of Graham Principles." In that letter, we noted that in a world of cryptocurrencies, SPACs (special purpose acquisition companies), and meme stocks, focusing on long-term thinking, seeking a margin of safety, being diversified, and having a keen focus on investment versus speculation sounded old-fashioned and disconnected from the so-called new normal that was prevalent in 2022. We argued then, and we argue now, that Graham’s principles are as enduring and relevant today as they were when he first wrote them.4

While there will always be innovation and technological advancements in our business, human nature, fear and greed will always be inexorably linked with investing. Graham understood this profoundly when he wrote:

"The investor’s chief problem—and even his worst enemy—is likely to be himself.”

With the advancement of robo advice and now generative AI, we will concede that these technologies can and most likely will provide reasonable investment advice. However, what we’re not sure about is whether the typical investor will always follow that advice to the letter. We think that this is precisely what Graham was alluding to when he talked about the investor’s greatest enemy. The best investment plan in the world is of little use if the investor abandons it at the first sign of trouble. This is why we believe that a simple, understandable investment approach is more likely to be adhered to over time. And adherence, over time, is a big determinant of the results achieved.

We’ve been investing client money since 1974. We know how hard it is to stick to a solid investment strategy. We know that our style can be out of favor for long periods of time. We know that one can look silly following a strategy that is not working in the short term. We know the pressure of hearing "this time it’s different."5 That’s why we have built our firm the way we have: independent, no star managers, and based on an approach that has been honed over decades. All these are designed to keep us focused on being consistent, reliable practitioners of value investing.

Over the years, our investment approach has been criticized as being too simplistic, even quixotic. We’ve had to defend ourselves, especially during periods when our style was out of favor. However, we believe consistency is a core part of our edge and one of the key factors driving our long-term results.

We encourage you to evaluate our approach versus the many approaches available in today’s complex market.

In a world that celebrates complexity and the allure of quick riches, we remain steadfast in our belief that a reliable path to building long-term wealth is, perhaps ironically, one that is not very exciting: value investing—buy good businesses at reasonable prices, be patient, stay disciplined, and let the power of compounding do its work. We believe there is enduring value in that simplicity—which we sometimes refer to as a “get rich slowly” approach.

Thank you for your continued trust.

Oliver Murray1 Source: Callan LLC, The Callan Periodic Table of Investment Returns, Year-End 2025. The Periodic Table depicts annual returns for 9 asset classes, ranked from best to worst performance for each calendar year. A key overarching takeaway is that no single asset class outperforms in every environment. In 2025, all listed asset classes generated positive returns, with International and Emerging Market equities leading. Past performance is not a guarantee of future results.

2 Lester, Ashley, Luis O'Shea, and Patrick Warren, "Has Private Equity Outperformed Public Equity?", The Journal of Private Markets Investing, Fall 2025, Volume 24, Number 1. The study uses MSCI's private-capital universe covering 14,453 funds and nearly USD 12 trillion in committed capital. Buyout direct alphas of 3.8% (pooled, net of fees and carry) are measured against a subindustry-adjusted, levered version of the MSCI USA Small Cap Index. For vintages since 2000, buyout outperformance was 2.9% and venture capital was −0.4%.

3 Eugene F. Fama and Kenneth R. French, “Luck versus Skill in the Cross-Section of Mutual Fund Returns,” The Journal of Finance, Vol. 65, No. 5 (October 2010), pp. 1915–1947.

4 Brandes Investment Partners, Brandes Letter, March 2022, "The Enduring Value of Graham Principles." Graham quotes drawn from The Intelligent Investor by Benjamin Graham (Fourth Revised Edition, with commentary by Jason Zweig, HarperCollins, 2003). Chapter 1: "Investment versus Speculation: Results to Be Expected by the Intelligent Investor."

5 Quote widely attributed to Sir John Templeton: “The four most dangerous words in investing are: ‘This time it’s different.’” Alpha: A measure of performance based on the excess return of an investment relative to the return of a benchmark index. Margin of Safety: Discount of a security’s market price to what the firm believes is the intrinsic value of that security.

Click here for the Brandes Global Equity GIPS Report. Performance for all Brandes strategies can be found at Brandes.com.

Past performance is not a guarantee of future results. All investments carry a certain degree of risk including the possible loss of principal.

This material is for informational purposes only. It should not be assumed that any security transactions, holdings, or sectors discussed were or will be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance discussed herein. Strategies discussed are subject to change at any time by the investment manager in its discretion due to market conditions or opportunities. Market conditions may impact performance. The performance results presented were achieved in particular market conditions which may not be repeated. Moreover, the current market volatility and uncertain regulatory environment may have a negative impact on future performance. The Brandes investment approach tends to result in portfolios that are materially different than their benchmarks with regard to characteristics such as risk, volatility, diversification, and concentration.

International and emerging markets investing is subject to certain risks such as currency fluctuation and social and political changes; such risks may result in greater share price volatility. Such risks are increased when investing in emerging and frontier markets. Additional risks associated with emerging and frontier markets investing include smaller-sized markets, liquidity risks, and less established legal, political, social, and business systems to support securities markets. Some emerging and frontier markets countries may have fixed or managed currencies that are not free-floating against the U.S. dollar. Certain of these currencies have experienced, and may experience in the future, substantial fluctuations, or a steady devaluation relative to the U.S. dollar.

Diversification does not assure a profit or protect against loss in a declining market. Intrinsic value estimates can change over time. The MSCI World Index with net dividends captures large and mid cap representation of developed markets.

The MSCI World Value Index with net dividends captures large and mid cap securities across developed market countries exhibiting value style characteristics, defined using book value to price, 12 month forward earnings to price, and dividend yield.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice. Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.